BRIDGING TRENDS: bridging activity down in Q1

Gross bridging lending activity slowed in the first quarter of 2017, according to the latest Bridging Trends data.

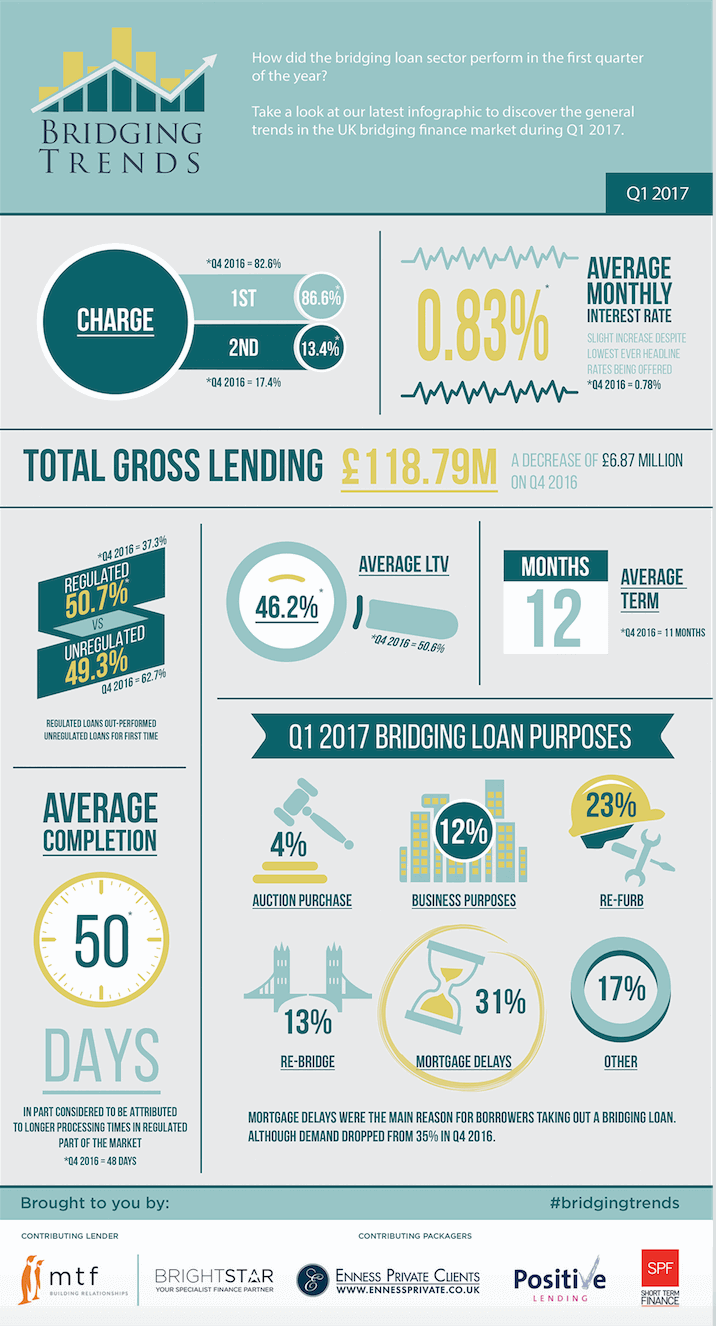

Data from Bridging Trends revealed contributor gross lending reached £118.79 million in the first quarter of 2017, constituting a 5.5% decrease on Q4 2016 (£125.66 million). The figure is also down on the corresponding data for Q1 2016 by 5.23% (£125.35 million).

Bridging Trends is a quarterly publication conducted by bridging lender MTF, and specialist finance brokers Brightstar Financial, Enness Private Clients, Positive Lending, and SPF Short Term Finance, designed to monitor the general trends in the bridging finance market.

Regulated bridging loans outperformed unregulated bridging loans for the first time since Bridging Trends was launched (April 2015). The number of regulated loans transacted by contributors increased from 37.3% in Q4 2016 to 50.7% in Q1 2017.

Mortgage delays were again the most popular reason for the use of a bridging loan in Q1 2017 at 31% of all lending, dropping from 35% during Q4 2016. Refurbishment was again the second most popular reason for getting a bridging loan contributing to 23% of all lending.

First charge lending for the quarter rose to 86.6%, from 82.6% during Q4 2016. Second charge transactions dropped slightly from 17.4% in the previous quarter, to 13.4%.

Average LTV levels dropped to 46.2% in Q1 2017 whilst the average monthly interest rates were up to 0.83%, representing an increase of 0.05% on the previous quarter.

The average completion time on a bridging loan application increased by 2 days to 50.

The average term of a bridging loan hit a new high at 12 months.

The significant swing towards regulated lending marks an interesting shift which, in turn, we consider has impacted the average time it takes to complete a bridging loan. Also, whilst the level of regulated activity is up it is interesting to see rates increase for the first time in 5 reporting cycles.

Whilst it is too early in the year to draw any firm conclusions from this first quarter of data, it is these key parameters we are most keenly observing as we move forward in the year.

For more information, please visit www.bridgingtrends.com