Simplifying complexity: Bridging made effortless

In the fast-paced world of specialist finance, ‘complexity’ is often inevitable and could most likely slow things down unnecessarily and in the world of bridging…

Bridging in 2024 – A year of efficiency and adaptation

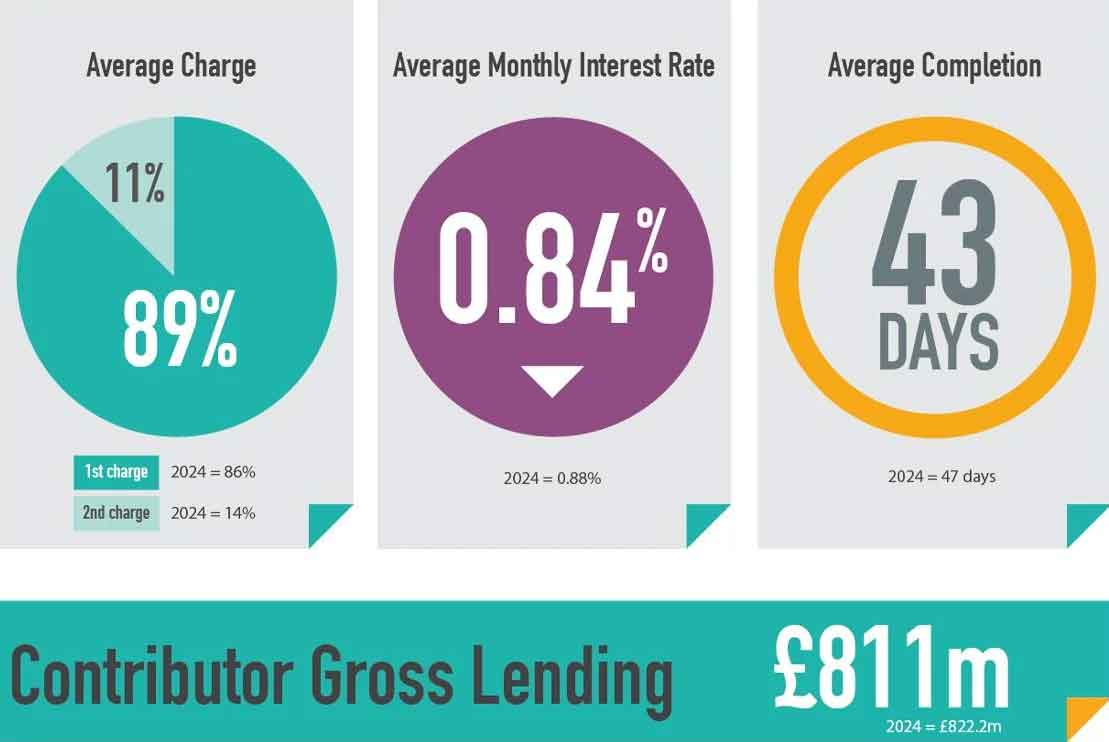

Throughout the year, lending volumes remained consistent at £822.2 million, despite economic uncertainty. This consistency speaks to the resilience and constant evolution of the market.…

Bridging completion times hit eight-year low in 2025

The 2025 annual Bridging Trends data was released today, and the headline news is a significant leap in efficiency for the short-term finance industry. According…

Bridging lending hits £209.4m in Q3 as demand increases

As borrowers remain cautious about the upcoming Autumn Budget – and what’s going to happen to the base rate – many are turning to specialist…

Navigating commercial complexity with ease

By Gareth Lewis, Deputy CEO at MT Finance As the commercial property landscape continues to evolve, successful commercial mortgage deals require more than just competitive…

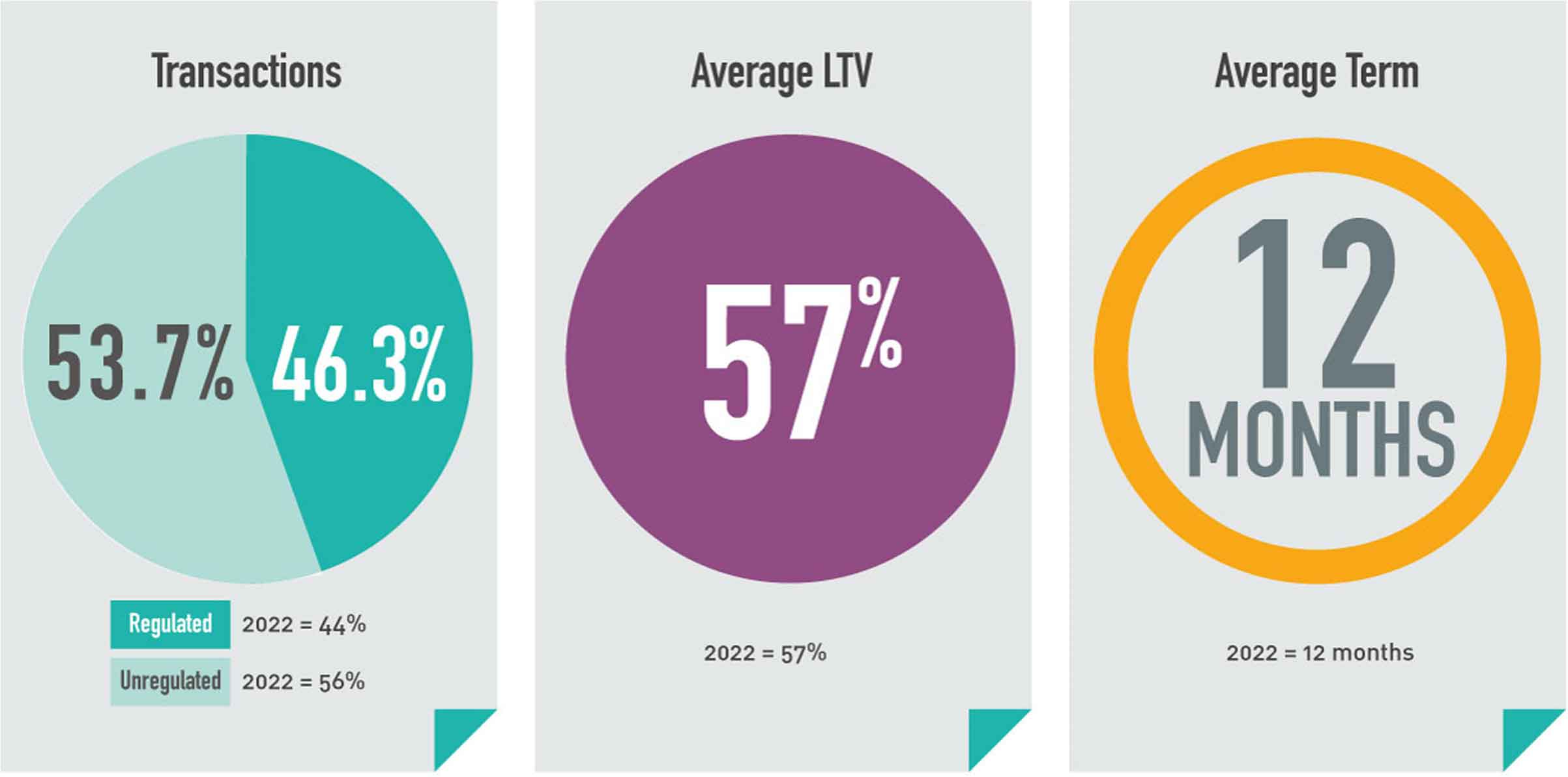

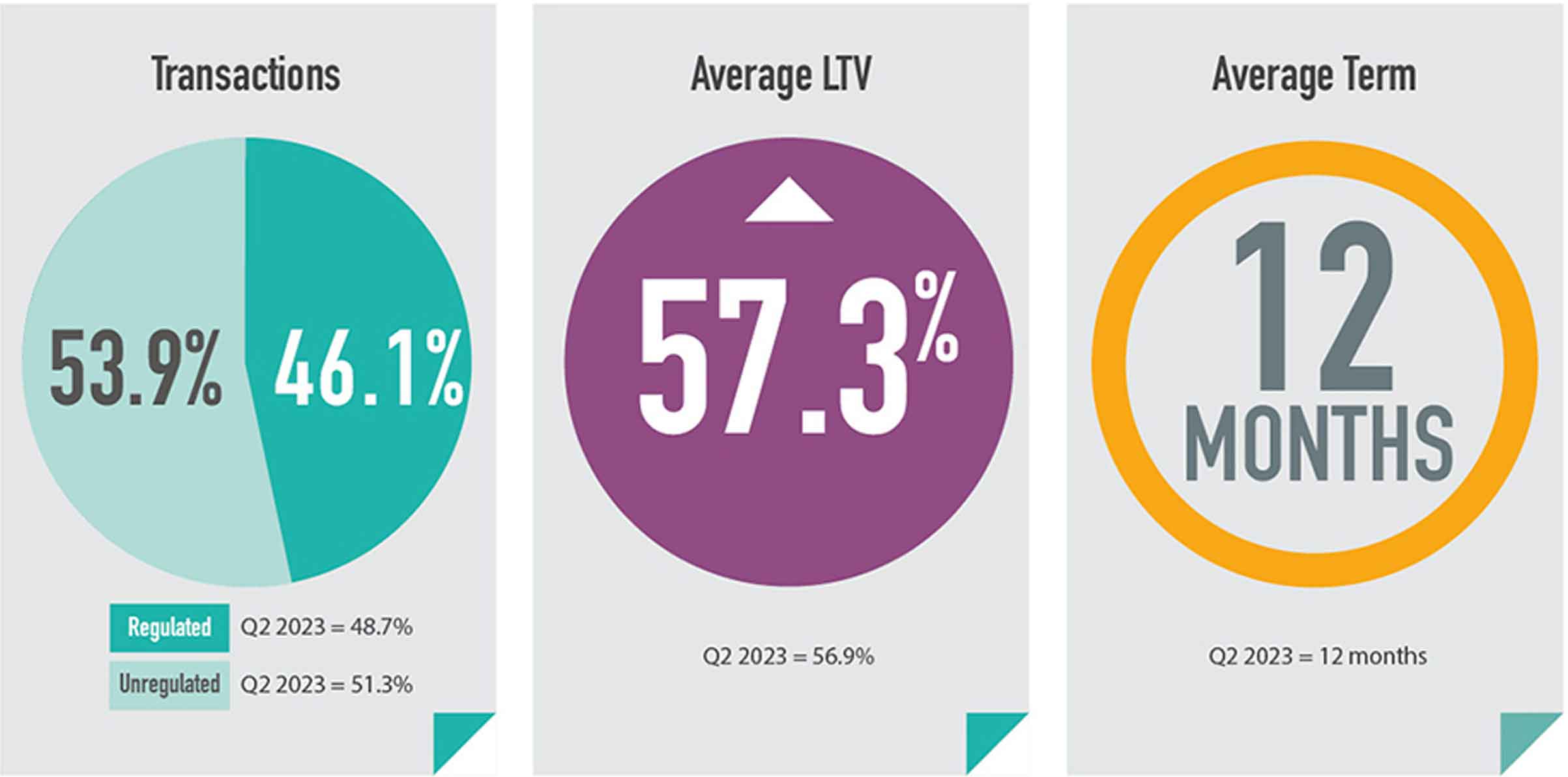

Bridging Trends Q2 2025: Market shows continued stability

The Q2 2025 Bridging Trends report shows a period of resilience and stability, with key indicators pointing to an increasingly competitive and mature sector. Here’s…

Unlocking potential from a multi-unit commercial property

As the commercial real estate landscape continues to evolve, many property investors are leaning into the significant opportunities commercial mortgages provide. At MT Finance, we…

Commercial mortgages: A new era in lending

Commercial property investment offers compelling opportunities with higher yields and greater stability than residential alternatives and as the landscape continues to evolve, we understand that…

Bridging Trends Q1 2025 shows stability and adaptability

The UK bridging finance market has shown significant stability and adaptability in the first quarter of 2025, according to the latest Bridging Trends data. Despite…

Making a difference: Supporting Goods for Good charity

At MT Finance, we believe in the power of community and the importance of giving back. That’s why we were proud to dedicate our support…

A Comprehensive Guide to Buy-To-Let Mortgages

A buy-to-let (BTL) is a mortgage taken out when an individual purchases a residential property specifically to rent it out to tenants rather than live…

A Comprehensive Guide to Bridging Finance

Bridging finance is a short-term loan designed to ‘bridge’ a financial gap until a long-term funding solution can be arranged. These loans are typically secured…

MT Finance marks International Women’s Day 2025

In honour of the global International Women's Day celebrations, MT Finance hosted a special team luncheon providing an opportunity to connect, reflect, and celebrate the…

Bridging in 2024 – A year of efficiency and adaptation

Throughout the year, lending volumes remained consistent at £822.2 million, despite economic uncertainty. This consistency speaks to the resilience and constant evolution of the market.…

We have added new product offerings to our buy-to-let range

As the Buy-to-Let market continues to face headwinds from rate and regulatory changes, the role of specialist lenders has become increasingly vital. The current landscape,…

Simplifying complexity: Bridging made effortless

In the fast-paced world of specialist finance, ‘complexity’ is often inevitable and could most likely slow things down unnecessarily and in the world of bridging…

Bridging market outlook 2025: Trends and opportunities

Market review: looking back at 2024 The bridging finance sector demonstrated remarkable resilience throughout 2024, adapting to shifting market dynamics and evolving borrower needs. At…

Bridging market defies slowdown with record-breaking Q3

MT Finance compiles Bridging Trends, a quarterly index that compiles data from 12 of the UK's leading finance brokers. In Q3, the contributors recorded faster…

Health Hour recap: MT Finance x Prevent Breast Cancer

October is Breast Cancer Awareness Month, a time to raise awareness, provide support to women with breast cancer and highlight how early screening can significantly…

Maximising quick turnarounds for time bound purchases

In the fast-paced world of property investment, opportunities come and go in the blink of an eye. This is especially true for below market value…

How can a second charge bridging loan help your client?

With the recent lowering of both buy-to-let and residential mortgage rates, savvy landlords and investors are turning to their existing assets to help raise capital.…

Bridging lending continues to increase in Q2 2024

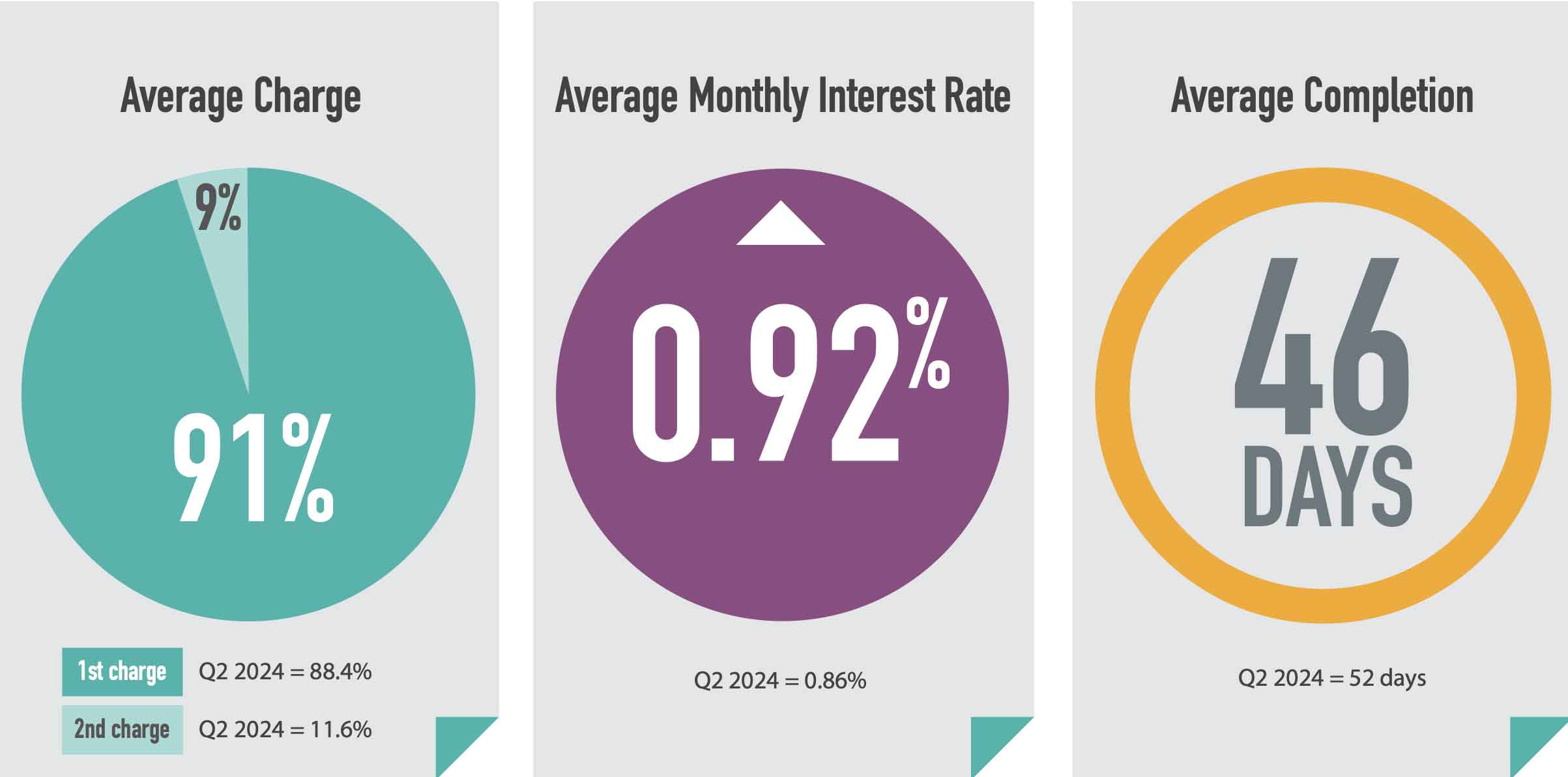

Released earlier today, the Q2 2024 Bridging Trends data shows that contributor gross lending rose for the fourth consecutive quarter. Hitting £201.8 million, this is…

What we’re doing to beat the infamous summer lull

The weather may not be quite up to scratch but there’s no denying that summer is well and truly here – if only in spirit.…

Countdown to the general election: What the experts say

As the general election approaches, it is crucial for the next government to prioritise the housing and property market. We turned to four industry experts…

How will the general election impact the property market?

As we approach the upcoming general election, many of your clients may be concerned with its impact on the property market. After all, any major…

Ngage Finance’s co-founders on why giving back matters

Making a difference requires determination, and that is exactly what director, Gareth Lewis and BDM, David Kingham showed when they joined forces with Ngage Finance…

Bridging Trends reveals sector certainty in Q1 2024

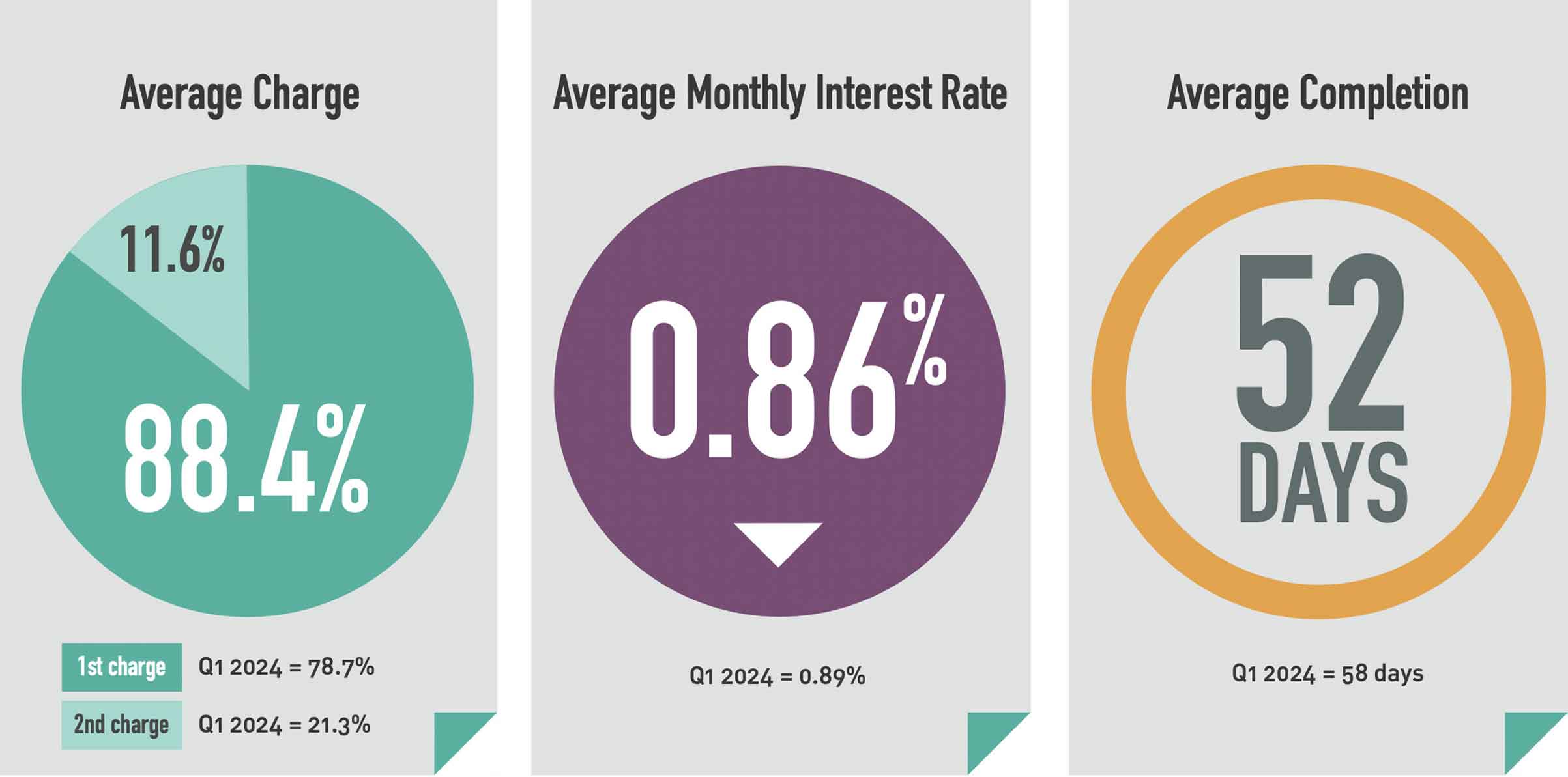

This morning, the Q1 Bridging Trends data was released and revealed a consistent performance of gross bridging lending in Q1 2024 – a strong indicator…

Maximising rental ROI: How specialist finance can help

As both tenants and landlords continue to face financial pressures, the arguments for and against rental increases show no sign of letting up. With the…

MT Finance marks International Women’s Day 2024

Today (Friday 8th March) marks 2024’s International Women’s Day. Created to both celebrate women’s achievements and raise awareness about what is needed to drive gender…

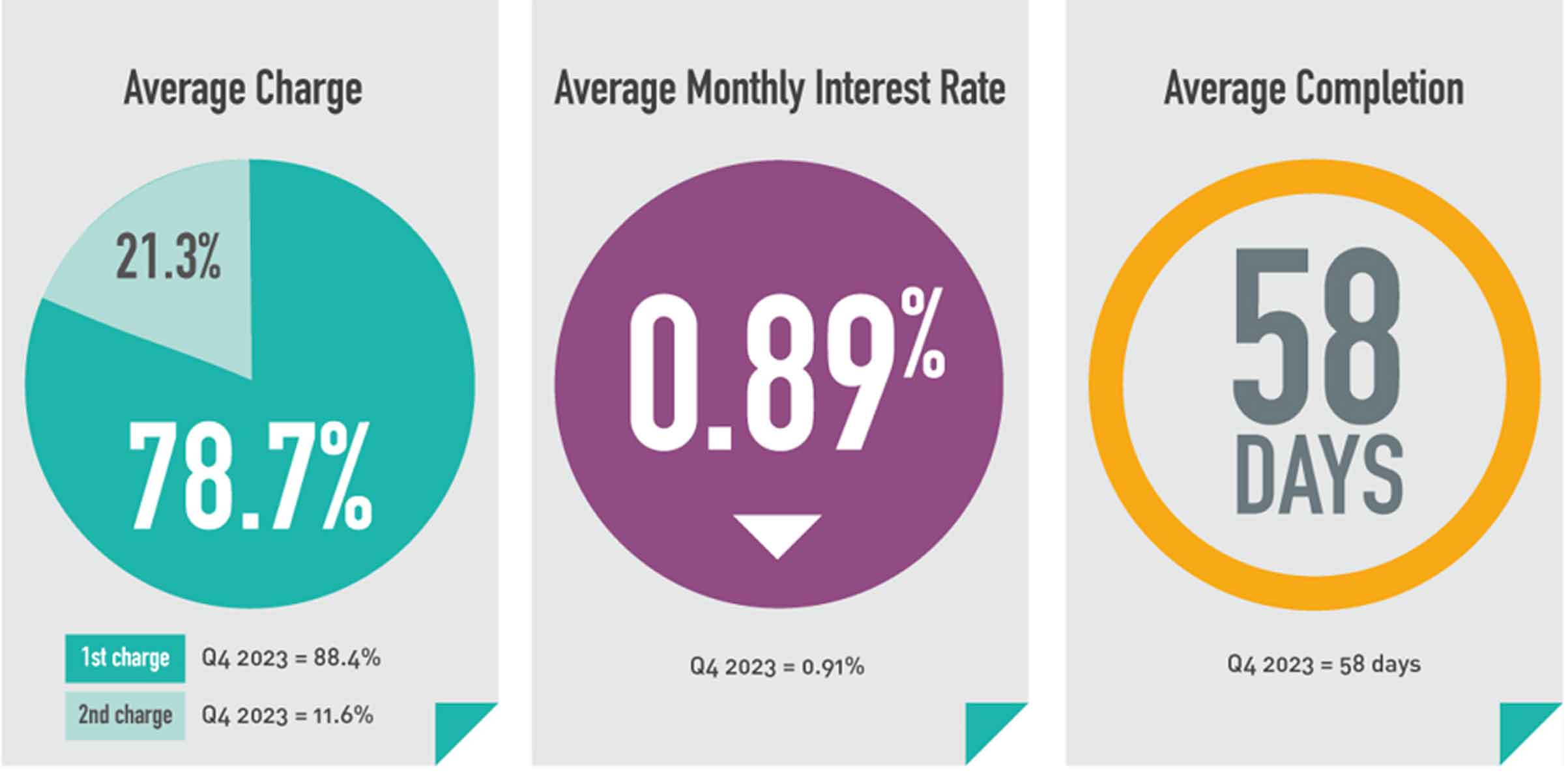

Annual bridging loan transactions hit record high in 2023

2023 may have been marked by ups and downs but as the economic outlook remained uncertain for much of the year, an increasing number of…

We’ve added AVMs to our bridging finance range

In the 15 years since MT Finance was launched, we have never stood still. From new products to new departments, we are always looking at…

Is now a good time to diversify? The pros and cons to consider

The issue of affordability continues to dominate the conversation for many landlords. Those looking to remortgage or purchase a new rental property may face significantly…

Bridging loan transactions increase to £191 million in Q3

The latest Bridging Trends data is in and has revealed a 15.3% spike in bridging loans transacted by contributors* during the third quarter of 2023.…

How specialist BTL is supporting landlords with affordability

For many landlords, the issue of affordability is one that continues to dominate conversation. As the Bank of England base rate remains high (at least…

Will the EPC U-turn make it better in the long run?

Back in September, Rishi Sunak announced a series of changes to the government’s green commitments. Among these included the scrapping of Energy Performance Certificate (EPC)…

Interest rates remain at 5.25% as MPC halts further rise

The Bank of England’s Monetary Policy Committee has made a big decision – after 14 consecutive rate rises, they have voted to keep interest rates…